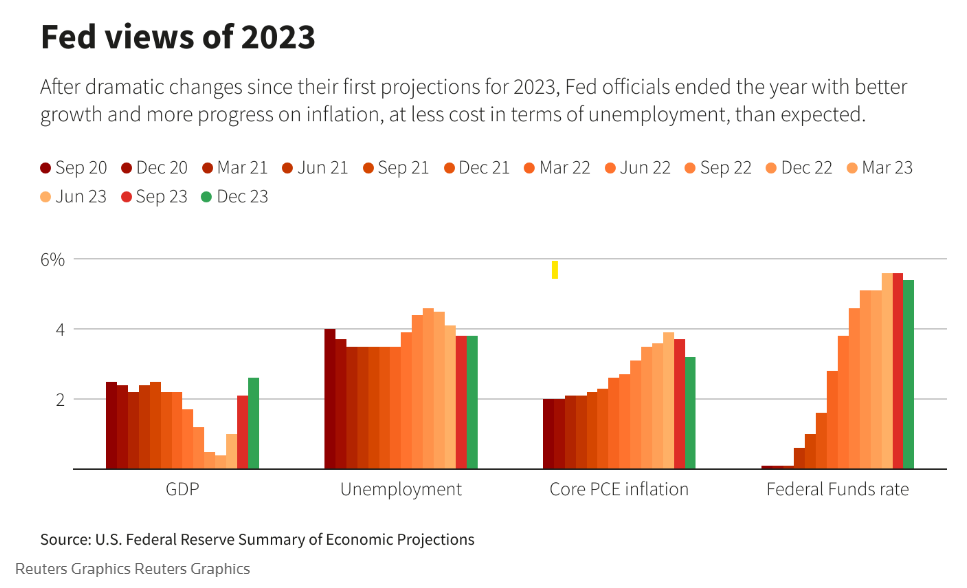

WASHINGTON – The U.S. Federal Reserve started 2023 on a grim note, with staffers calling a recession “plausible,” and policymakers penciling in growth near stall speed and rising unemployment as the costs of quashing inflation with rapid-fire interest rate increases.

But it ends with the Fed registering faster-than-expected progress on inflation that occurred with virtually no rise in the jobless rate and an economy that grew fully five times faster than the 0.5% policymakers anticipated a year ago. Rate cuts are now in the offing.

“We were very fortunate,” over the course of the year, Atlanta Fed President Raphael Bostic told Reuters last week.

What just happened?

Over the year a series of things turned the Fed’s way, sometimes unexpectedly and not necessarily due to monetary policy. Just as 2022 was a year of bad forecasts and bad breaks, including war in Europe, the 2023 economy began looking more normal after pandemic-era excesses. It redeemed, to some degree, early Fed thinking that high inflation would ease over time without the central bank squelching growth altogether.

Actions taken by the Fed included an emergency lending program for banks that helped ease financial sector tensions at a key point. There were also legitimate surprises like a rise in productivity, and other developments tied to the economy’s underlying performance, like the increase in the labor force.

“Institutions have evolved and opportunities have become sufficiently attractive that people have come back in strong. I was not expecting that. That’s very positive,” Bostic said.

The forecasts still weren’t great through an uncertain and volatile period. But this time the surprises were mostly to the good.

MONEY FOR NOTHING, CHIPS FOR A FEE

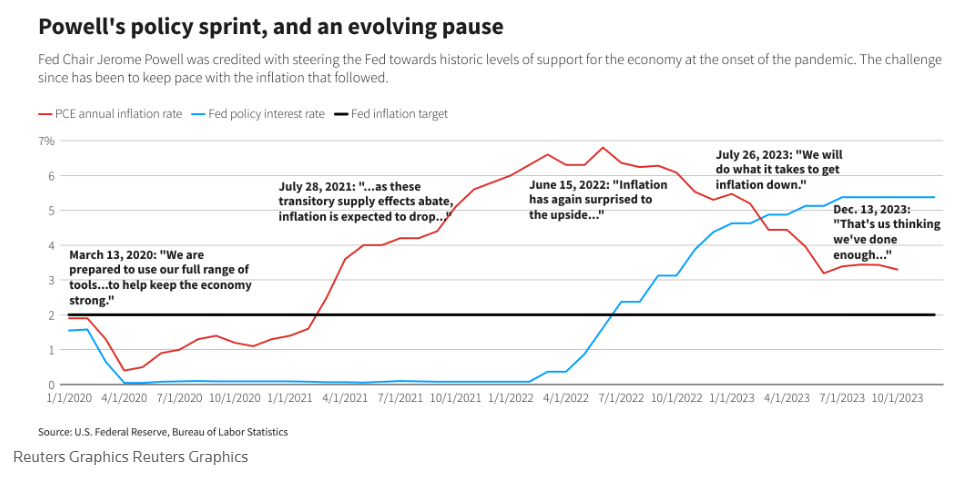

Fed Chair Jerome Powell stopped using the word “transitory” to describe inflation long ago, but last week he described, without saying it, why that belief took hold.

The pandemic had dumped trillions of dollars of aid into consumers’ hands, stoking demand that hit a wall as the global goods supply chain became stilted by that same pandemic. Shortages of basic industrial goods like computer chips kept inventories bare and allowed rising prices to ration what was available.

This year saw supply pressures unwind as inventories rebuilt, perhaps to excess. Goods prices began to drag headline inflation lower, as was often the case before the pandemic.

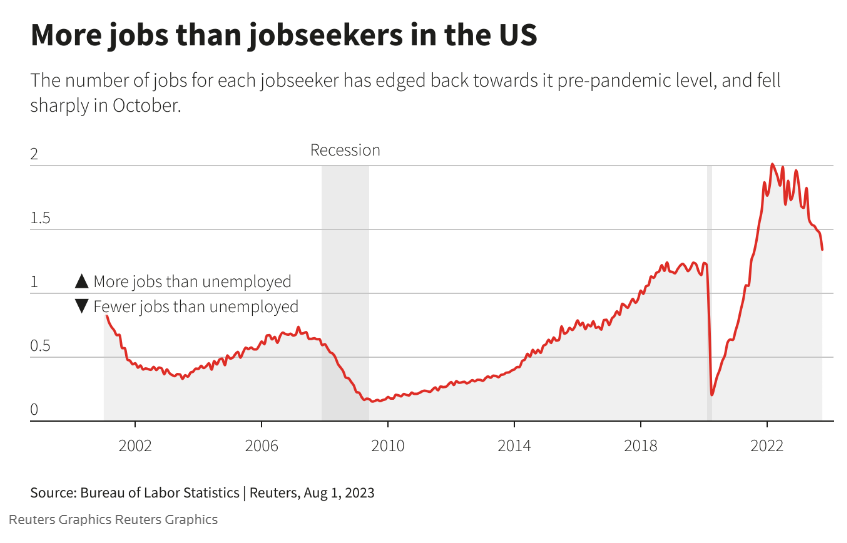

Labor supply also surprised to the upside. After concerns early in the pandemic that women’s ability to work had been permanently scarred, the number of women in the workforce hit a record high. Rising immigration helped even out what had been a historic mismatch between the number of open jobs and the number of people looking for work. The boost in the labor force and drop in job openings have helped slow wage growth that some top economists worried was on the verge of driving inflation higher.

HOUSEHOLDS HOLD THE FORT

While the gusher of pandemic aid may have helped push up prices from high demand, the financial buffers built by households and local governments had more staying power than many economists expected. Over 2023, long after pandemic benefit programs had ended, there were still estimates of hundreds of billions of dollars left to spend.

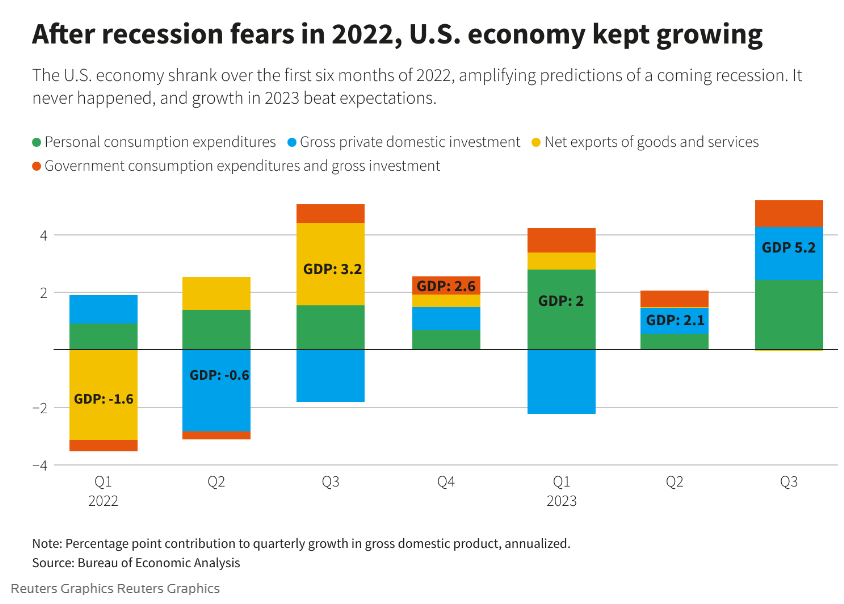

That showed up in consumer spending that consistently beat expectations. Though recent data suggests demand has finally begun slowing, the surprising resilience of household spending was a key reason the Fed’s initial growth forecasts proved low.

A PRODUCTIVITY BONUS

All things equal, that unexpectedly strong jump in gross domestic product should be inflationary. The Fed estimates the economy’s underlying growth potential is around 1.8% annually, so 2023’s estimated 2.6% expansion seems out of kilter.

But “potential,” at least for now, may have been lifted by a jump in worker productivity. Rising productivity is manna for central bankers, allowing faster growth without inflation because each hour of work yields more goods and services at the same cost.

It is also something they are reluctant to predict or rely on. In this instance, however, it helped Powell drop what had been steady references to the “pain” needed to subdue inflation through rising unemployment and instead talk more openly of the relatively pain-free disinflation apparently underway.

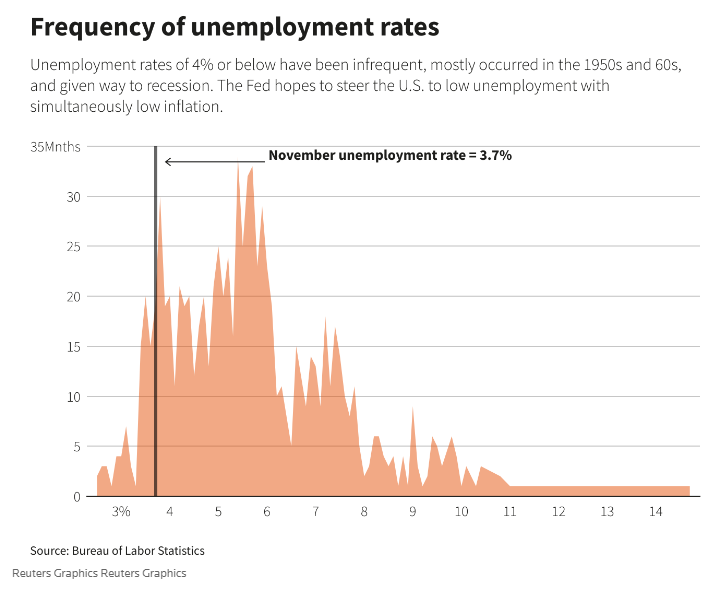

Today’s unemployment rate is 3.7% versus 3.6% when the Fed began raising interest rates. It has been below 4% for 22 months, the longest such run since the 1960s, and roughly what prevailed just before the pandemic, a period Powell heralds frequently.

THE BANKING CRISIS THAT WASN’T

A final surprise is how contained the spring’s round of bank failures proved to be after the rapid collapse of Silicon Valley Bank. Those tremors prompted new caution among Fed policymakers about the speed of further rate increases, and led to warnings of a deep financial fracture as banks took stock of the fact their holdings of government and mortgage securities had lost value due to Fed rate hikes.

Certainly there was stress. But it didn’t evolve into a broader crisis and stayed in line with what the Fed was trying to do anyway: Tighten credit to cool the economy.

Indeed, following what proved to the Fed’s last rate increase in July, markets began doing some of the central bank’s work for it by driving borrowing costs higher than the Fed anticipated doing with its own rate.

Market rates are now falling, some dramatically, as the Fed pivots towards rate cuts. Will the markets go too far?

Fed officials are conscious of the time it takes for changes in financial conditions to work into the real economy. Recent weeks have seen increases in loan delinquencies and other signs of household stress, while there was also worry about the amount of corporate debt that needs to be refinanced, and the trouble that could cause companies if rates are unaffordable.

The Fed’s “soft landing” scenario won’t be assured unless the central bank, as Powell noted, doesn’t “hang on too long” to its current restrictive policy.

“We’re aware of the risk,” Powell said last week.

WILL THE GOOD NEWS CONTINUE?

Powell also said he thought some of the forces working in the Fed’s favor, particularly supply improvements, have “some ways to run.”

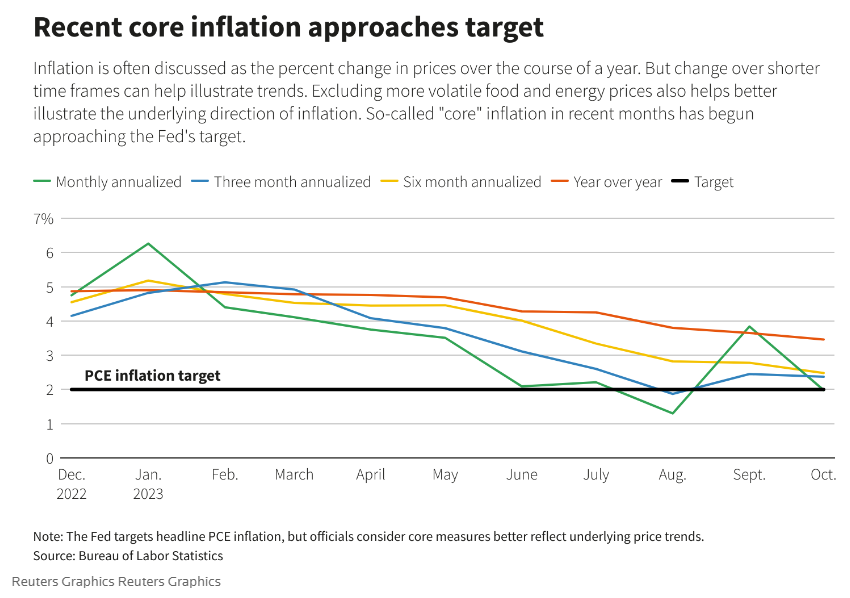

Inflation for the past half year has only been about 2.5%, with strong arguments for it continuing to fall.

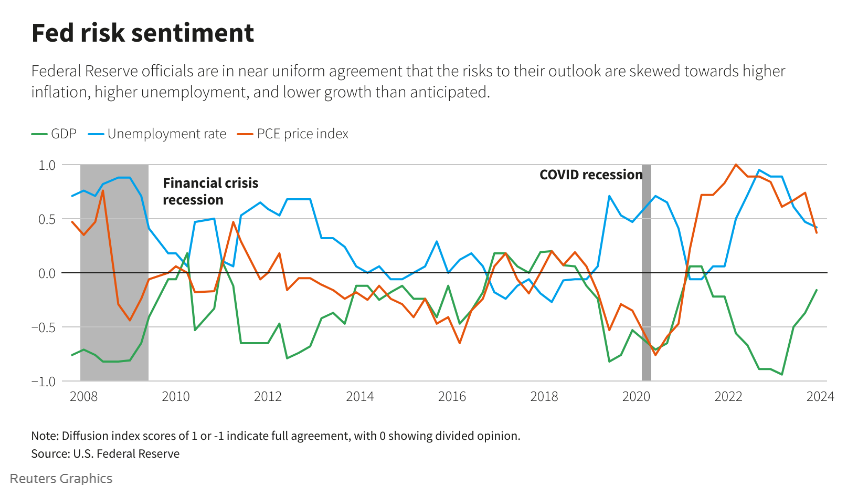

In the Fed’s most recently released policy documents, officials tucked in a subtle statement about their faith in the economy’s return to normal. An index of risk sentiment fell towards a more balanced view, with inflation even seen by a number of officials as more likely to fall faster than to move higher.

Spectrum Wealth Management, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Additional information about Spectrum’s investment advisory services is found in Form ADV Part 2, which is available upon request. The information presented is for educational and illustrative purposes only and does not constitute tax, legal, or investment advice. Tax and legal counsel should be engaged before taking any action. The opinions expressed and material provided are for general information and should not be considered a solicitation for purchasing or selling any security.