March 6, 2023

When it comes to retirement savings, there is a disparity among different genders. Women have historically saved less for retirement than men. This is due to a number of reasons, including a gender wage gap. Having less in savings leads to a delayed retirement and longer working years. Women also tend to live longer than men, which means they should be saving even more.1

KEY TAKEAWAYS

- Women typically have less money saved for retirement than men.

- Women generally earn less than men and can have career gaps due to caregiver roles that can lead to lower savings, lifetime wages, and Social Security.

- A lack of financial and educational opportunities leads to lower financial literacy among some women, resulting in delayed retirement savings plans.

- Improving access to financial education will help improve savings across genders.

- Continuing to close the gender wage gap and potential policy changes could help bolster retirement savings potential.

Retirement Savings: Men vs. Women

The disparity in retirement savings between women and men is striking. A study conducted by the Transamerica Center for Retirement Studies estimates that the median retirement savings for women is $43,000, less than half of men’s ($91,000). Men are much more likely than women to have $250,000 or more in retirement savings—32% compared to 21%. The study also found that 25% of women have saved less than $10,000, or nothing at all, compared to 16% of men.2

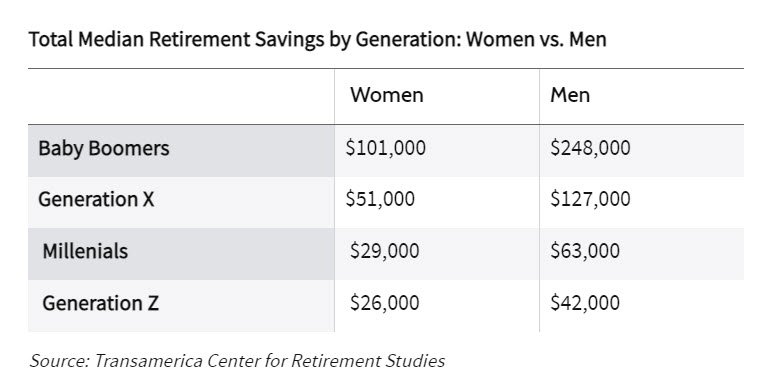

The below chart shows the difference between the median retirement savings of men and women by generation:

IMPORTANT:

The COVID-19 pandemic threw a big wrench into retirement savings planning, with some 4 million people in the U.S. out of work for six months or longer.3

Women sustained more damage than men in terms of job losses.4 The impact was felt even more deeply by transgender people.5 These painful realities will likely be felt for years to come.

Why a Retirement Savings Gender Gap Exists

There are a number of reasons why women have historically socked away less for retirement. One big driving force behind the savings disparity is the wage gap. Though it has been improving, women are still only paid an average of 83 cents for every $1 that men make.6

There is no any readily available wage comparison data for trans people or nonbinary members of the trans community as of February 2023, including on Social Security. We do know the outlook is also challenging for trans people, who often face even wider wage gaps in comparison to their cisgender counterparts.

Lower wages mean there’s less left over to save for retirement. Women are also more likely to have gaps in employment for taking time away from the workforce to have a child or care for a relative, leading to lower benefits when it comes to calculating Social Security.7 On average, men collected $1,838 per month in Social Security in 2021, versus $1,484 per month for women.8

16%: How much taking time off from the workplace to have a child reduces a woman’s Social Security payout, according to research by the Brookings Institution. Taking time off to care for an elderly relative can cut lifetime Social Security earnings by $131,000.1

Another reason why the retirement savings gap has persisted is a lack of financial literacy. Knowledge is power, and never has that been truer than when it comes to retirement savings. Women lag behind men in financial literacy, according to a 2020 report from the Global Financial Literacy Excellence Center.9 The reasons for this include feeling uncomfortable when talking about money and not knowing where to go to be better informed. Additionally, financial planning and investment advising have generally been skewed more toward men.

How to Narrow the Gender Retirement Savings Gap

Steps can be taken to narrow the retirement savings gap. It starts with financial literacy. Without the knowledge of how and why to save, it can be an uphill battle to even get started. Start early. You’re never too young to learn about money and saving. There’s a wealth of information out there to help anyone interested in getting their savings plan started or keeping it on track.

For those who take time off to have a child or to care for a relative—and those who work part time at jobs that don’t offer savings plans—there are changes at the policy level that could help.1 One way is to create a paid family leave act at the federal level. Though the Family and Medical Leave Act (FMLA) provides workers with 12 weeks of unpaid leave, only nine states and Washington D.C. have any paid leave policies in place.10,11

And though the wage gap has narrowed, it will likely require some major policy changes to really move that needle. One country did just that. Iceland began requiring companies with 25 employees or more to report that they pay the same wages for men and women or face daily fines.12

In the U.S., President Joe Biden outlined an ambitious plan to tackle some of the financial disparities between men and women, starting with the creation of the White House Council on Gender Equality.13

How Long Will Retirement Savings Last?

How long your retirement savings will last depends on a number of factors including your living expenses after you retire, how much you have in retirement savings and income, and how long you live. One rule of thumb, called the 4% rule, suggests that if you don’t want to outlive your savings (assuming you live 30 years after retirement) you can withdraw about 4% of your retirement savings annually, in addition to retirement income such as Social Security. For example, if you plan to withdraw $40,000 a year for 25 years, you would need $1 million in your nest egg.

What Is the Average Retirement Savings?

The average IRA balance at the end of 2022 was $104,000, a 36% increase from 2012, according to research published by Fidelity. The average 401(k) balance came close at $103,900, up 34% from 2012. Fidelity also reports that the average 403(b) account balance was $92,683 at the end of last year, a 56% increase from 2012.14

How Do You Start Saving for Retirement?

You can start saving for retirement by contributing to a tax-advantaged retirement plan or account. If you work for an employer that offers a 401(k) plan, contributions can be automatically deducted from your paycheck. If you don’t have access to a 401(k), you can set up and make contributions to a traditional IRA, a Roth IRA, or both.

The Bottom Line

It’s a vicious cycle. Though the wage gap is narrowing, as noted above, women still only earn about 83 cents for every $1 a man makes. And, as also mentioned above, lower wages translate to lower savings, which impacts how much will be available in retirement.

Closing the gender wage gap and implementing policy changes could help bolster retirement savings for all people in the U.S. Improving financial literacy will also help.

This article was originally published in Investopedia on March 6, 2023, and written by Catherine Tymkiw.

1. https://www.investopedia.com/retirement-savings-by-gender-5100948

2. Image courtesy of iStock

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

Article Sources

1. The Brookings Institution. “How Does Gender Equality Affect Women in Retirement?”

2. Transamerica Center for Retirement Studies. “Emerging from the COVID-19 Pandemic: Women’s Health,Money, and Retirement Preparations.”

3. The White House. “Remarks by President Biden on the State of the Economy and the Need for the American Rescue Plan.”

4. National Women’s Law Center. “All of the Jobs Lost in December Were Women’s Jobs.”

5. Human Rights Campaign and PSB Research. “The Economic Impact of COVID-19 Intensifies for Transgender and LGBTQ Communities of Color,” Page 2.

6. AAUW. “The Gender Pay Gap.”

7. National Committee to Preserve Social Security & Medicare. “Women and Retirement: The Gender Gap Persists.”

8. Social Security Administration. “Fast Facts & Figures About Social Security, 2022,” Page 20.

9. Global Financial Literacy Excellence Center. “Financial Literacy and Wellness Among U.S. Women.”

10. U.S. Department of Labor. “Family and Medical Leave Act.”

11. National Conference of State Legislatures. “Paid Family Leave Resources.”

12. Government of Iceland. “Equal Pay Certification.”

13. White House. “Gender Policy Council.”

14. Fidelity. “Fidelity 2022 Retirement Analysis: In The Midst of Inflation and Uncertainty, Retirement Account Balances Are Rising.”

Spectrum Wealth Management, LLC is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Additional information about Spectrum’s investment advisory services is found in Form ADV Part 2, which is available upon request. The information presented is for educational and illustrative purposes only and does not constitute tax, legal, or investment advice. Tax and legal counsel should be engaged before taking any action. The opinions expressed and material provided are for general information and should not be considered a solicitation for purchasing or selling any security.